Agricultural credit score stipulations within the 10th District moderated in the second one quarter and farmland values persevered to extend.

Agricultural credit score stipulations within the 10th District moderated in the second one quarter and farmland values persevered to extend. Following more than one years of substantial growth, farm source of revenue softened, and borrower liquidity retracted quite along persevered value pressures and decrease costs for many agricultural commodities in comparison to a yr in the past. Even supposing value will increase were extra modest in 2023 than closing yr, many agricultural lenders anticipated mortgage call for to extend and reimbursement charges to say no in coming months. In spite of sharp will increase in rates of interest and a notable slowdown in money rents, farmland values nonetheless grew at a powerful tempo.

In spite of some moderation, the 10th District’s farm economic system used to be secure in the second one quarter. Drought early within the quarter adopted by way of heavy rains later contributed to issue with iciness wheat harvest and spring planting. Some agricultural bankers commented that diminished grain costs, climate volatility, and solid manufacturing bills may just scale back borrower liquidity that were very sturdy all over renewal season. Upper rates of interest have additionally greater borrowing prices for farmers, however mortgage call for has remained solid, and financial institution liquidity remained sound regardless of a slight pullback in deposit balances.

Credit score Stipulations

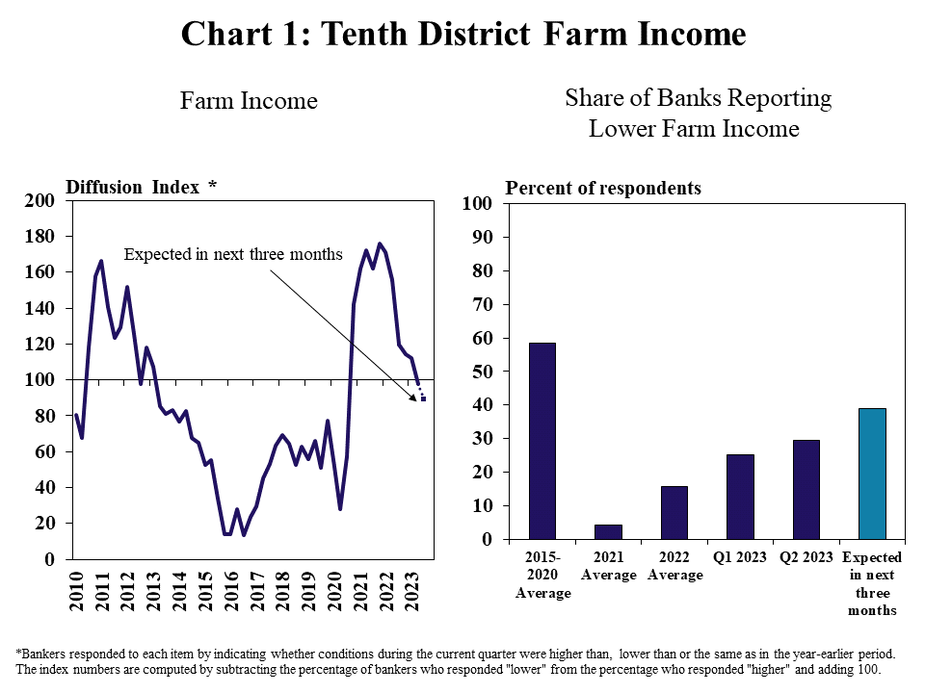

Farm earning within the 10th District have moderated along extra tempered stipulations within the agricultural economic system. The adjustments in farm source of revenue around the area had been flat in the second one quarter following two years of substantial energy (Chart 1). The proportion of lenders reporting that farm earning had been less than a yr in the past rose for the fourth consecutive quarter, and greater than a 3rd of respondents expected weaker stipulations than closing yr within the subsequent 3 months.

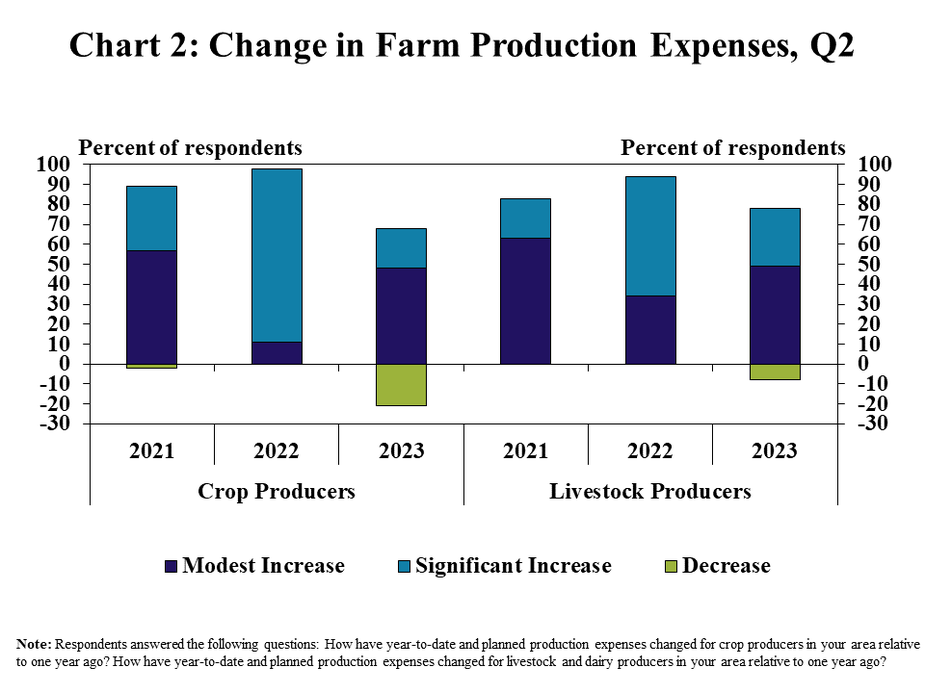

Source of revenue expansion has flattened along increased manufacturing bills, however value pressures confirmed indicators of easing. Neatly over part of respondents reported that manufacturing bills for all sorts of manufacturers persevered to extend, however the level of build up used to be significantly extra modest than closing yr (Chart 2). Prices for crop farmers declined within the lending spaces of 20% of banks, whilst discounts in prices for cattle manufacturers had been extra restricted.

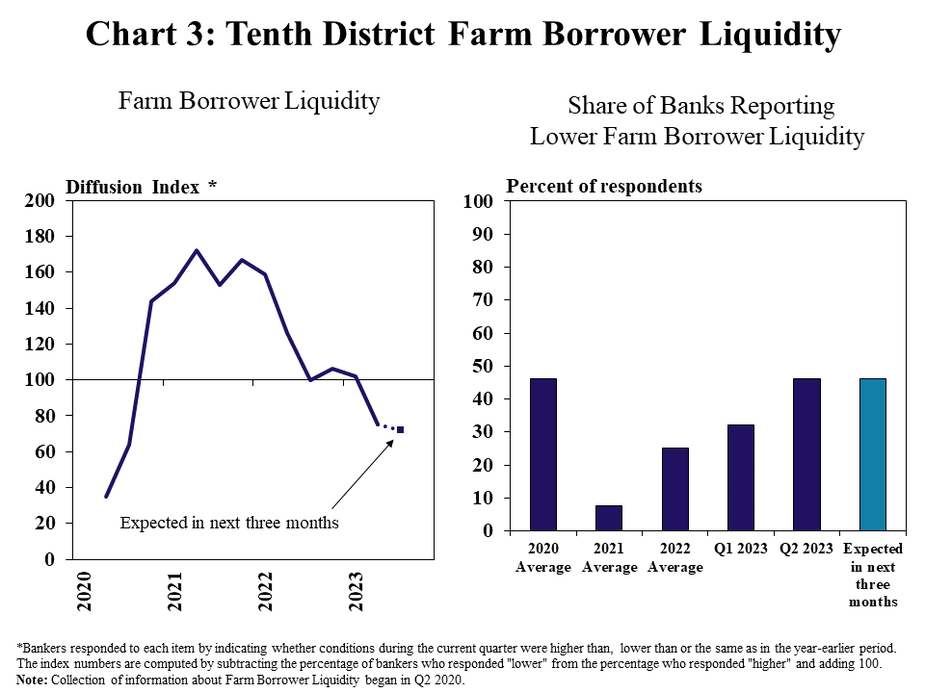

Expense pressures and a moderation in commodity costs have lowered farm liquidity within the area. Farm borrower liquidity declined at a reasonable tempo in the second one quarter for the primary time since 2020 (Chart 3). Just about part of respondents reported that manufacturer money reserves had been not up to the similar time a yr in the past, and a an identical charge of decay used to be anticipated within the subsequent quarter.

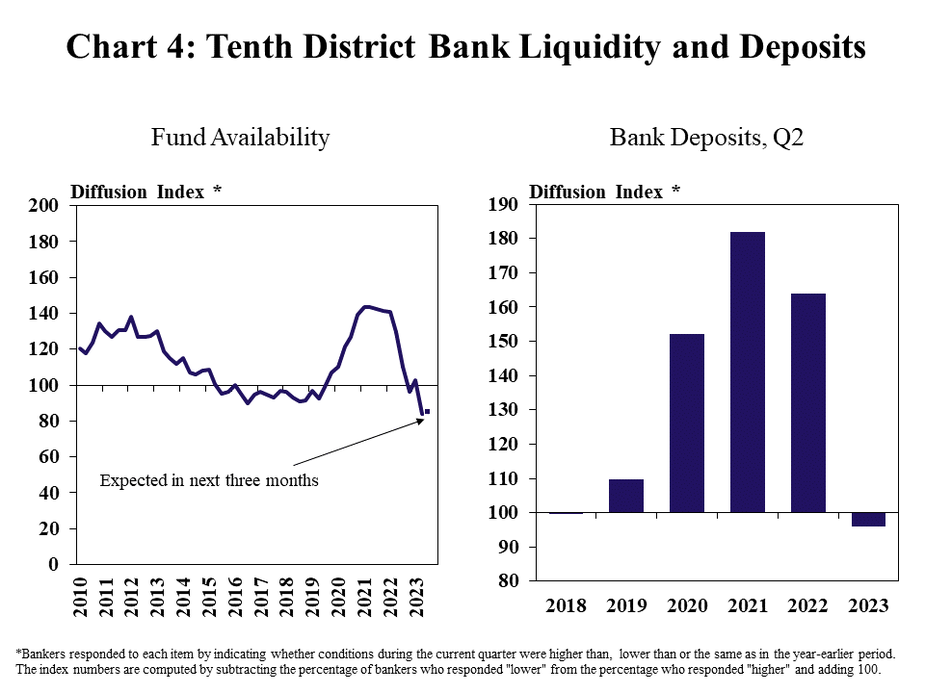

Financial institution liquidity has additionally retracted moderately in contemporary months as deposit expansion has eased. Availability of budget declined at a modest tempo in the second one quarter following vital expansion the previous 2 years (Chart 4, left panel). Deposit balances had been not up to a yr in the past for plenty of lenders, however liquidity at agricultural banks has remained sound following a number of years of sturdy deposit expansion and subdued mortgage call for (Chart 4, proper panel).

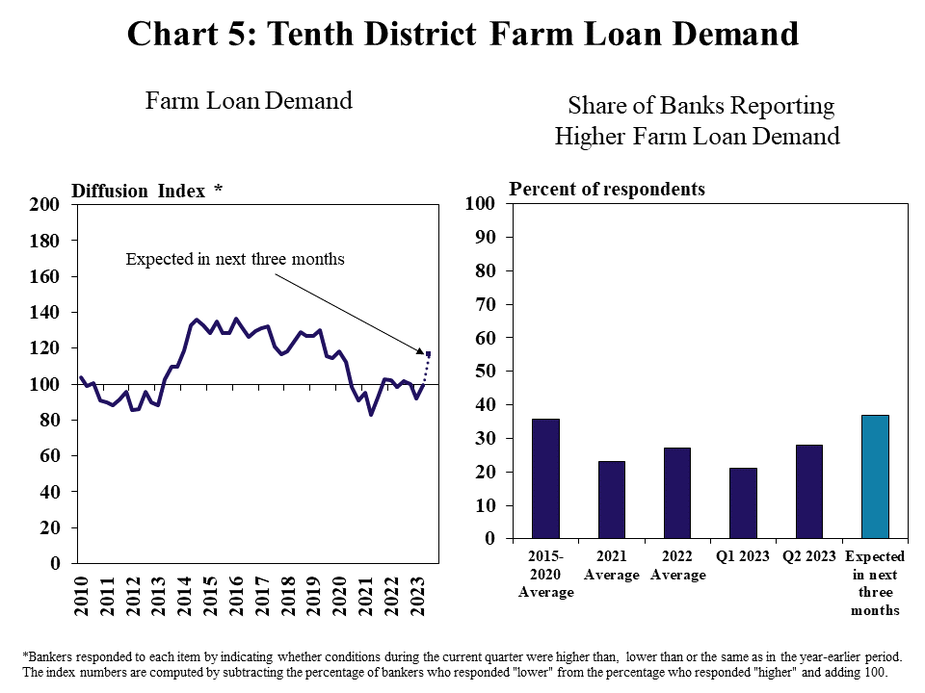

Mortgage call for within the District remained flat, however some bankers persevered to be expecting a rebound along increased prices and up to date liquidity depletion. Call for for non-real property farm loans used to be just about unchanged around the area, with kind of 1 / 4 of banks reporting will increase and reduces from a yr in the past (Chart 5). Upper manufacturing prices have driven up credit score wishes for some debtors, whilst many others have applied money holdings to complement mortgage balances and scale back passion bills.

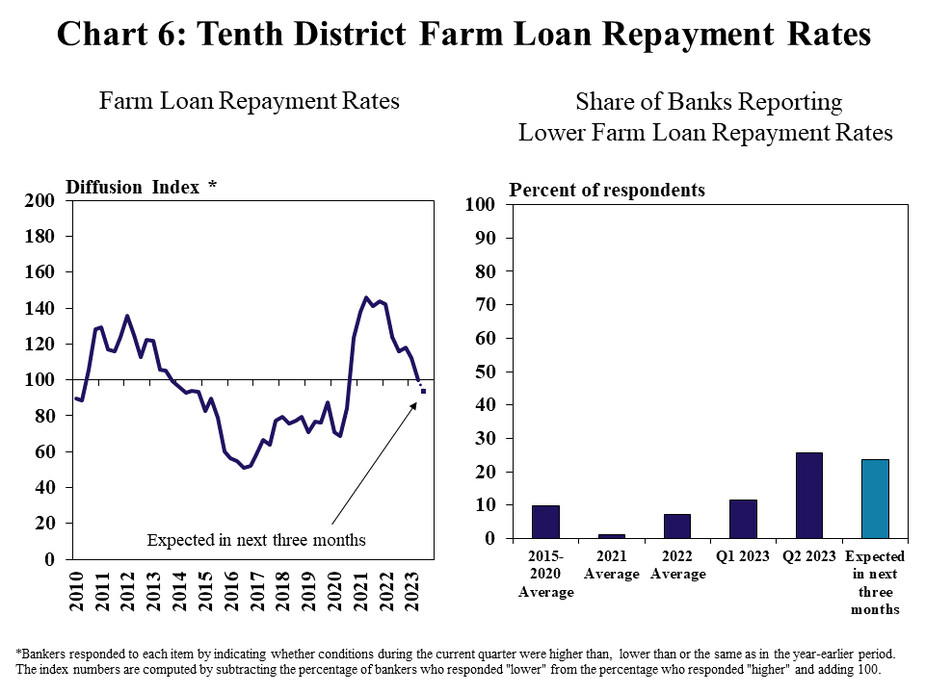

Very similar to farm source of revenue, growth in farm mortgage reimbursement charges has additionally moderated in contemporary months. Adjustments in farm mortgage reimbursement charges had been flat in the second one quarter following really extensive growth all over contemporary years (Chart 6). The proportion of banks reporting slower reimbursement reached the best stage since 2020 and a an identical percentage anticipated some slowing within the months forward.

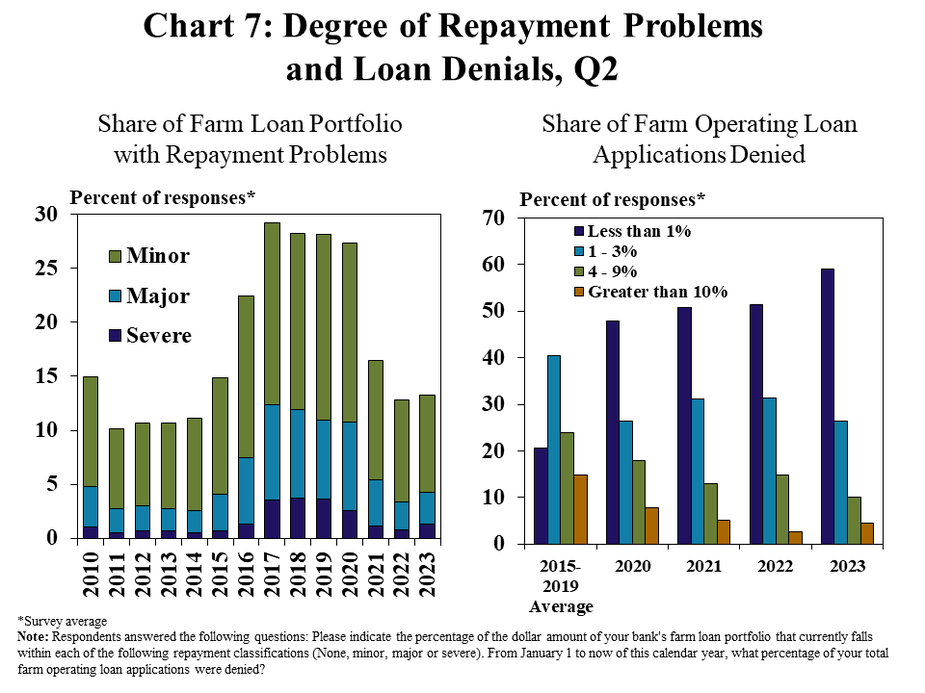

The level of reimbursement problems, then again, remained marginal thru the second one quarter. On moderate around the District, fewer than 15% of all farm mortgage balances had reimbursement issues and nearly all of problems had been thought to be minor (Chart 7). The large energy in agricultural credit score stipulations additionally saved the speed of denials on farm working loans at traditionally low ranges.

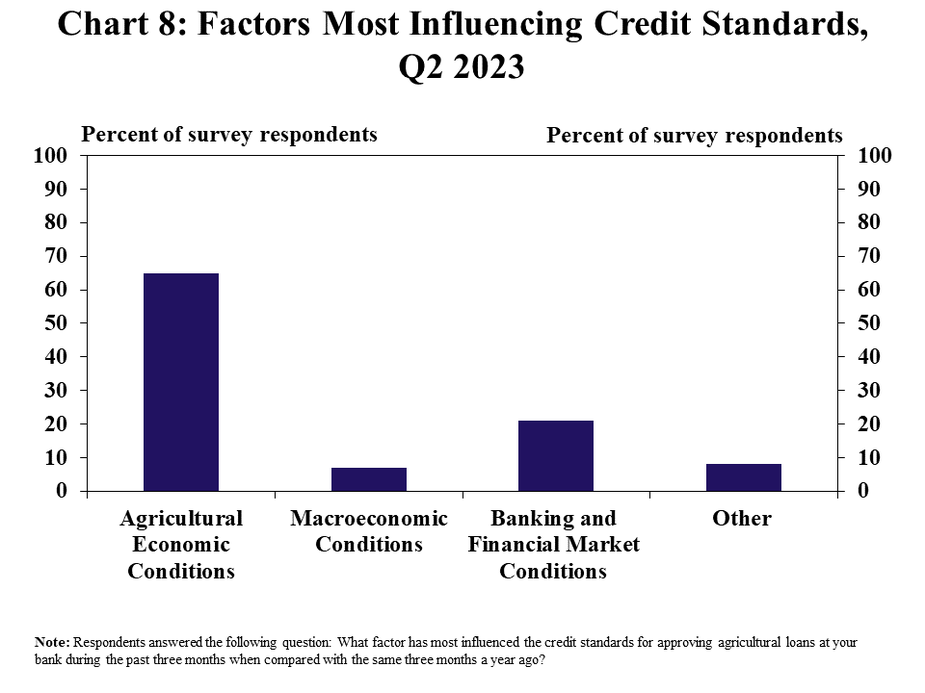

Stipulations within the farm economic system remained the main issue for figuring out credit score requirements for agricultural debtors, however banking and monetary marketplace stipulations had been extra vital for some lenders. About two-thirds of respondents indicated that agricultural financial stipulations had been probably the most influential elements in agricultural mortgage software selections (Chart 8). A smaller, however sizable 20% of banks thought to be broader banking and monetary marketplace stipulations crucial issue.

Hobby Charges and Farmland Values

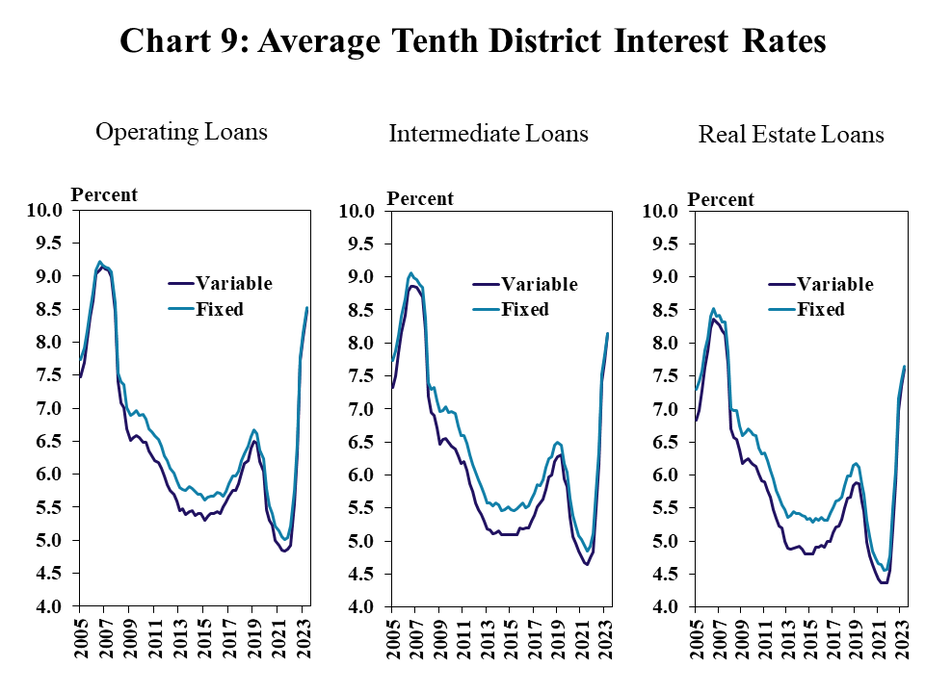

Reasonable rates of interest greater from the former quarter along additional will increase within the federal budget charge, and the unfold between variable and stuck charges narrowed. In the second one quarter, rates of interest on working and intermediate loans greater by way of about 40 foundation issues from the former quarter, and charges on genuine property loans had been greater than 3 proportion issues upper than in 2021 (Chart 9). Mounted charges have traditionally been upper than variable charges, in particular all over classes of charge relief, then again, variable and stuck charges had been just about equivalent for all mortgage sorts in the second one quarter.

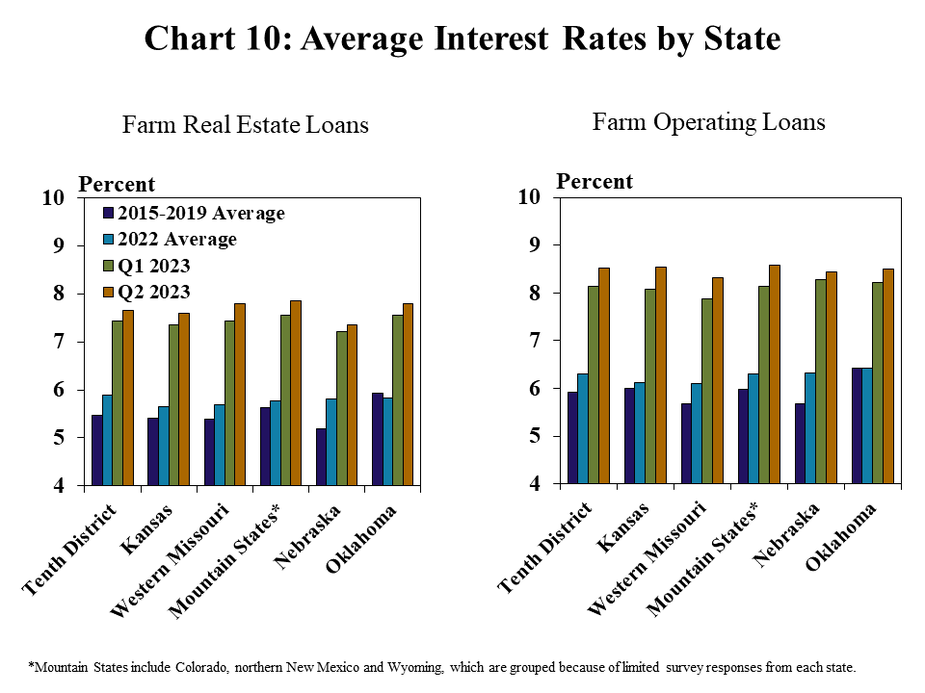

Rates of interest on farm genuine property and working loans have grown impulsively throughout all states. Ultimate yr, moderate rates of interest had been moderately above the pre-pandemic moderate in maximum states (Chart 10). In Oklahoma, moderate charges on farm genuine property loans had been moderately under the common from 2015 to 2019. On the other hand, the speed setting in 2023 has modified significantly for farm debtors, as rates of interest on working loans rose above 8 p.c, on moderate, in all states in the second one quarter.

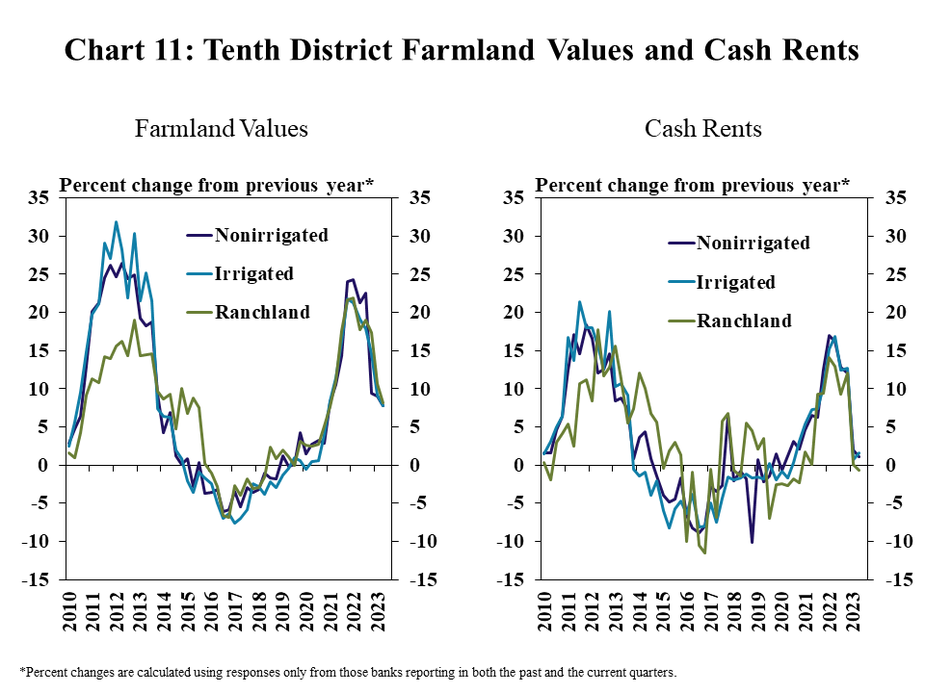

Enlargement in farm genuine property values remained reasonably sturdy regardless of the speedy upward thrust in rates of interest and a few moderation within the farm economic system. Values for all sorts of farmland grew by way of virtually 8 p.c in the second one quarter (Chart 11). Even supposing the common charge of expansion for nonirrigated cropland declined from greater than 20 p.c a yr previous, persevered energy in farmland markets has passed off along extra pronounced softening in money rents. Money rents for ranchland declined moderately for the primary time since 2020 in the second one quarter, and rents for cropland greater by way of only one p.c.

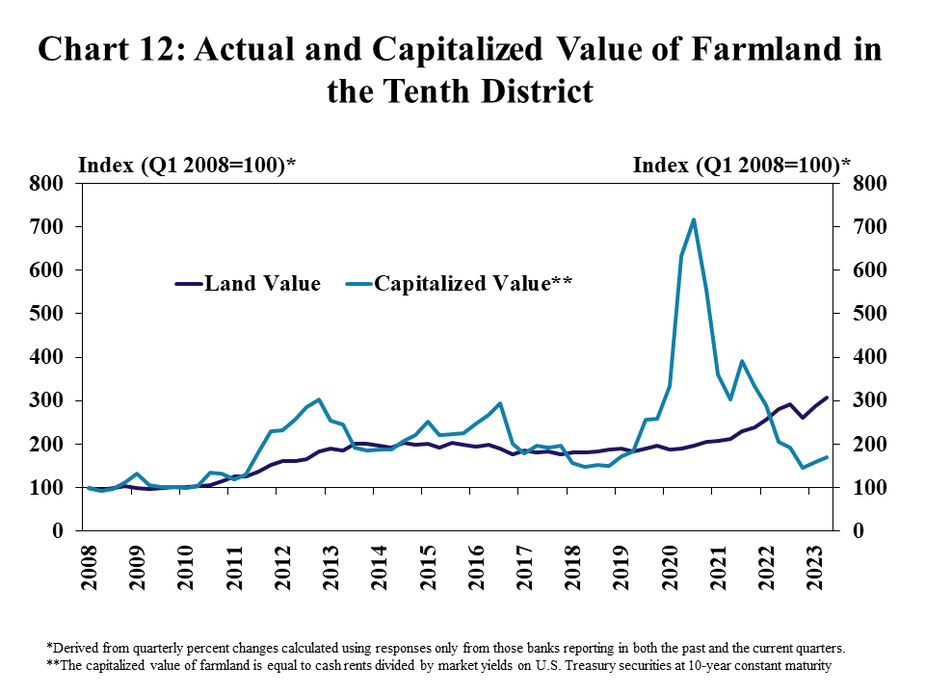

Substantial energy in farmland markets has driven values above what is also anticipated given the present rate of interest setting and possibilities for monetary returns from money rents. Reported values of farmland within the District have persevered to upward thrust regularly in contemporary months because the estimated price in accordance with the connection between money rents and benchmark rates of interest (capitalized price) has dropped significantly (Chart 12). Capitalization values supply a strategy to assessment the mixed results of rates of interest and returnsand have declined along the speedy build up in rates of interest and a moderation in money rents. Some moderation in farmland values may well be anticipated given those downward pressures, in particular for extra marginal or much less productive tracts, then again, a secure provide of land gross sales and robust call for from farmers has most probably supported large resiliency of genuine property values.

Banker Feedback Q2 2023

“Our house has been significantly impacted as a result of wildfire closing yr and this yr. It’s truly laborious to are expecting the way forward for land values at the side of farm animals gross sales as a result of ranchers are having to promote their herds as a result of the fires.”– Northern New Mexico

“Drought stipulations are making for a deficient wheat harvest. Rains in recent times have helped the spring crop possible.”– Southwest Kansas

“Potentialities for a mean to just right fall harvest are taking a look higher with contemporary rains, however upper rates of interest and greater manufacturing prices aren’t serving to and farm animals gross sales were lowered as many head had been offered because of drought and now not carried thru iciness.”– Central Kansas

“With the 60-year low farm animals stock, this marketplace is anticipated to stick sturdy and someone with grass is purchasing farm animals with expectancies of greater costs later q4.”– Northcentral Kansas

“Maximum farmers are in a just right monetary situation; then again, drought will impact everybody to a point with upper enter prices, top rates of interest and a serious drought are making this a difficult yr, however maximum farmers will paintings thru it.”– Central Missouri

“The drought is hitting us laborious. We’re seeing a number of cow-calf operators lowering herd dimension because of loss of hay manufacturing.”– Southwest Missouri

“Drought stipulations in the neighborhood have brought about forage issues for pork farm animals manufacturers and can be a large restricting issue going ahead for the ones manufacturers when figuring out whether or not to enlarge or scale back herd numbers.”– Northwest Missouri

“Cattle manufacturers are very positive with considerably upper calf costs this spring and early summer time and crop manufacturers are cautiously positive with grain costs these days presenting a possibility to marketplace crop at very successful ranges.”– Northcentral Nebraska

“At renewal time, farm consumers had very good steadiness sheet liquidity. 3 to 6 months later, then again, with diminished grain costs and dryness in our house, it’s imaginable {that a} noticeable quantity of this liquidity may just erode.”– Northeast Nebraska

“Land values are final top with just right call for for cropland. Upper rates of interest don’t appear to be affecting our native economic system at the moment.”– Southcentral Nebraska

“Rates of interest, apparatus prices, and working bills – particularly gasoline, fertilizer, feed, and almost all working bills have positioned greater power on farm/ranch profitability.” – Southeast Oklahoma

“Emerging prices for feed and fertilizer are primary issues for our house and general marketplace stipulations are expanding prices for stockers.” – Southwest Oklahoma

“Upper rates of interest have greater bills for farmers and in flip they’re borrowing much less cash.” – Southeast Oklahoma