Thirty-five days and 5 marketplace classes later, we go back to the subject of the industrial tendencies in Spanish swine manufacturing. The present state of affairs is radically other from the only on the time of writing the earlier remark.

We introduced that the pig value in Spain may just do not anything however move down, and it has. The query of when was once cleared up only a week after remaining month’s article.

In Spain, we now have observed 5 consecutive downward actions; from the memorable and ancient 2.025 we now have fallen to at least one.905. A drop of 0.12 €/kg are living. After 4 months of being on the restrict, the associated fee is gliding down – reputedly with out panic – on the lookout for a backside.

It’s attention-grabbing to take a look at what has came about all through this identical time frame in different markets (all of that have observed decreases aside from China):

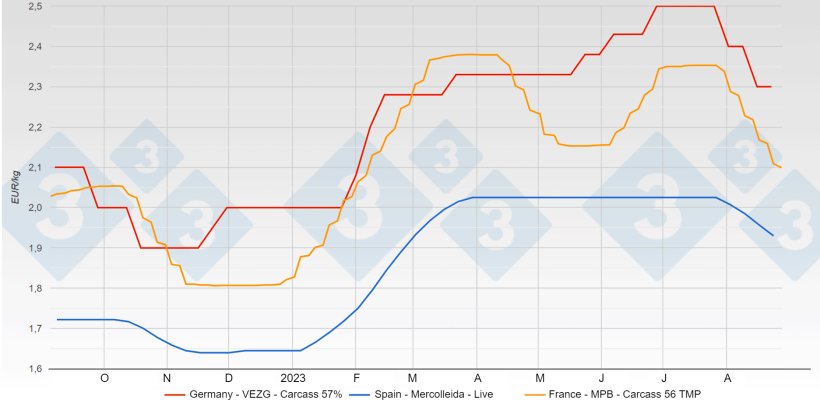

- In Germany, hogs are down from 2.50 to two.30, a drop of 0.20 carcass, similar to 0.152 €/kg are living.

- In France (historically Spain’s primary buyer) pigs have dropped from 2.35 €/kg carcass to two.05; a whopping 0.30 €/kg carcass similar to 0.23 €/kg are living.

- In Canada (Ontario) pigs have long past from 1.74 €/kg carcass to at least one.62; a lower of 12 cents carcass similar to about 0.09 €/kg are living.

- In the USA, hogs have dropped from 2.09 €/kg carcass to at least one.76: 0.33 €/kg carcass similar to 0.25 €/kg are living.

- In Brazil, they’ve long past from 1.27 €/kg are living to at least one.19. A drop of 8 cents/kg are living and nonetheless on the backside of the costs a number of the global’s main manufacturers.

- In China, the pig value has risen; from 2.09 €/kg are living on the finish of July to two.19 in mid-August. They’re emerging strongly and resolutely.

In Spain, pig costs are taking place, however extra quite than in Germany and particularly in France. In Canada and the USA, pig costs also are coming down after a obviously top month of July.

In China (finally!), pig costs appear to be emerging continuously. The principle cause for this upward push is none rather then the numerous slaughter of sows that has came about there. Allow us to remember the fact that, from the top of March to the top of July, the associated fee in China has been less than in Spain. The large losses (manufacturing prices in China are a ways upper than the ones in Spain) have pressured the foremost pig holders to cull sows whilst looking forward to higher occasions. Losses of loads of thousands and thousands of euros were reported in some massive Chinese language integrating corporations; their response to slaughter sows obeys the common sense of the marketplace.

In the USA, there are studies of neatly above-normal slaughtering of sows. Some massive manufacturers have reported multi-million buck losses and herd discounts. We predict higher costs within the close to long term.

The Spanish state of affairs -and due to this fact the Eu one- seems to be very complicated. Provide continues to be at a minimal, however intake has disappeared and exports to 3rd international locations are neither there nor anticipated. In consequence, there’s a surplus of red meat.

Let’s hope that the Rentrée (the go back of electorate to their houses after summer season holiday) will assist to mitigate the hunch by way of boosting intake. We concern that it’ll now not be sufficient, even though we want the entire assist we will get.

We will see a glimmer of hope within the distance; this present day it’s shaky and unsure, however it looks as if it’ll develop. We’re regarding the aforementioned lower within the Chinese language herd. It will rather well occur that during a couple of months, China’s red meat deficit will likely be important. We can have to attend and spot. In all probability the foreseeable lower in the USA may just additionally assist reinforce our exports in Spain.

In Spain, pig costs are reducing because of excessive marketplace fatigue. The slaughter capability a ways exceeds the are living provide. This circumstance interferes and a great deal influences the evolution of the associated fee. We will say that pig costs are taking place even if there isn’t a unmarried pig left over.

The lack of virulence of the essential PRRS lines in Spain nowadays is a reality. Piglets that turn out to be ill at the moment endure, however live on. Battered, however they live on. This reality may just result in an important build up in provide sooner than the top of the yr. We all know that the proscribing issue of the Spanish provide has been the presence of PRRS, since the entire breeding sows are nonetheless lively. We predict that during November lets see document slaughters once more.

The preliminary drops in pig costs in August have now not been handed directly to the red meat; even though slaughterhouses are nonetheless within the crimson, losses are not as critical as they have been on the finish of July.

It’s moderately conceivable that pig costs will move down till the weekly result of the slaughterhouses are balanced (to at least one.85? – to at least one.80?). A kind of company backside may just then seem that will grasp till past due autumn, when what we will believe as “regular provide” is available in. Despite the fact that, as is obvious, the whole lot is still observed.

We stay vigilant as to what occurs with a purpose to record on it.

In those unusual occasions, filled with turbulence, we want to recall a word from the nice German thinker Immanuel Kant: “The intelligence of a person is measured by way of the quantity of uncertainty he is in a position to undergo“.

Guillem Burset