Analyst Jim Wyckoff stocks international poultry information

14 july 2023

14 july 2023

16 minute learn

Chinese language meat imports upward thrust

China imported 670,000 MT of meat in June, up 12.1% from Might and 11.1% greater than final yr. China doesn’t spoil down the initial meat industry knowledge by means of class, however the building up used to be pushed by means of beef imports, that have been on the upward push since past due 2022. All the way through the primary part of 2023, China imported 3.81 MMT of meat, up 10.2% from the similar length final yr.

USDA Farm animals and Poultry: Global Markets and Business

Global Business Outlook Rather Unchanged Whilst Brazil Makes Features

The outlook for international meat industry stays slightly unchanged from the prior (April) forecast. Pork and white meat meat exports don’t seem to be considerably revised whilst beef is raised 2 p.c from the final forecast. Then again, Brazil continues to make export beneficial properties and set new data for pork, beef, and white meat meat. Brazil pork exports are revised 1 p.c upper to a few.1 million lots on higher manufacturing and company China call for. Brazil livestock costs have declined considerably in comparison to major competition – Uruguay and Argentina – and decrease pork costs give a boost to shipments to Southeast Asia, South The usa, and Center East markets. Brazil white meat meat exports are revised 2 p.c upper to 4.8 million lots on company shipments to Asia, the Center East, and smaller growing markets. As of July 12, Brazil stays freed from extremely pathogenic avian influenza (HPAI) in business operations and does no longer face restrictions as key competition do. Brazil beef exports are revised 8 p.c upper to one.5 million lots on sturdy exports to maximum Asia markets, together with in particular powerful shipments to China and Hong Kong. Declining feed costs in Brazil are expected to additional incentivize manufacturing and bolster worth competitiveness.

International pork manufacturing for 2023 is revised just about 1 p.c upper from the April forecast to 59.6 million lots. Drought has brought on extra herd liquidation in Argentina, elevating its manufacturing 6 p.c from the April forecast. In a similar fashion, higher feedlot placements and better cow slaughter are anticipated to spice up U.S. manufacturing by means of 1 p.c from April. New Zealand manufacturing is raised 3 p.c as male dairy calves are actually advertised for pork. EU manufacturing is minimize 1 p.c on decrease slaughter and lighter weights because of excessive enter prices.

International pork exports for 2023 are nearly unchanged from the April forecast at 12.1 million lots. Upward revisions within the forecasts for New Zealand, Australia, Argentina, and Brazil offset declines in forecasts for Mexico, United Kingdom (UK), and the EU. Company China call for is predicted to draw Brazil and Argentina shipments. Australia will have the benefit of emerging Japan and South Korea call for. As well as, powerful U.S. call for for processing pork will bolster Australia and New Zealand shipments. A strengthening peso weakens Mexico’s export outlook. Waning EU call for hampers UK exports whilst decrease EU manufacturing depresses EU shipments.

International beef manufacturing for 2023 is nearly unchanged from the April forecast at 114.8 million lots. Will increase within the manufacturing forecast for China, Canada, and Brazil offset declines in EU, Japan, the Philippines, and Mexico. In spite of most commonly destructive margins industry-wide, China manufacturing is upper on more than prior to now anticipated slaughter as manufacturers search to scale back herds and handle money float. EU manufacturing continues to wane because of power from environmental legislation, weaker intake, and slightly increased feed prices. Philippines beef manufacturing is decreased 3 p.c because of the growth of African swine fever in key manufacturing areas.

International beef exports for 2023 are forecast 2 p.c upper from the April forecast to ten.8 million lots as more potent shipments from the US and Brazil greater than offset declines from Canada, UK, and EU. Diminished EU beef provides supply alternatives for the US and Brazil to achieve marketplace percentage in different Asia markets together with South Korea and the Philippines. Sturdy call for from China has benefited maximum primary beef exporters yr to this point.

International white meat meat manufacturing for 2023 is little modified from the April forecast at 103.5 million lots. Manufacturing by means of Brazil, EU, and China weren’t revised on a endured outlook for stepped forward feed costs and as no primary outbreaks of extremely pathogenic avian influenza (HPAI) were reported. • International white meat meat exports for 2023 are raised not up to 1 p.c from the April forecast to 13.8 million lots. Shipments by means of Brazil are revised 2 p.c upper to 4.8 million lots on more potent shipments to Asia, the Center East, and smaller non-traditional markets. Brazil growth is supported by means of the absence of HPAI in business operations, aggressive costs, and intensive product choices satisfying the desires of more than a few markets. Thailand is raised 5 p.c upper to one.1 million lots on expanding shipments of raw white meat meat to Asia together with Japan, China, and South Korea.

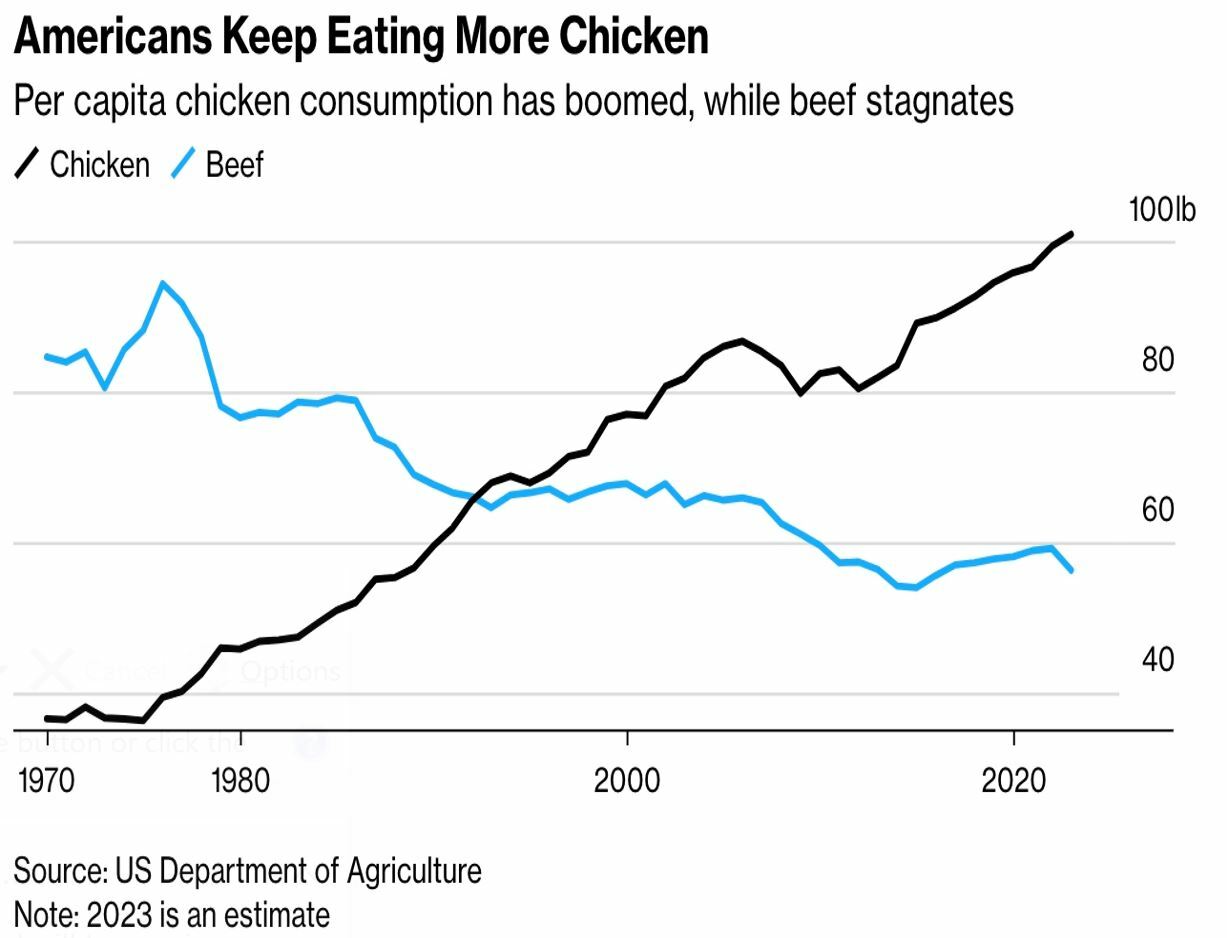

$85 billion U.S. pork {industry} is lately challenged by means of a robust choice for white meat

A contemporary Bloomberg article says the worry of festival from plant-based meat choices proved to be out of place as they hang a small marketplace percentage. The actual festival comes from white meat, which overtook pork in per-person intake in 1993, and the space continues to widen.

Hen’s affordability, 3 times less expensive than pork, and flexibility give it an edge over pork. Its recognition has higher very much because of its use in house cooking, processed meals, and eating places. In spite of well being and environmental considerations related to pork, the meat {industry} has struggled to rebrand and innovate.

David Maloni, a supply-chain marketing consultant, urged that reversing this declining pattern could be difficult given its long-standing nature. The sphere faces a couple of problems together with expanding feed prices, drought, and festival, decreasing income and perilous extra hardships with a cooling economic system.

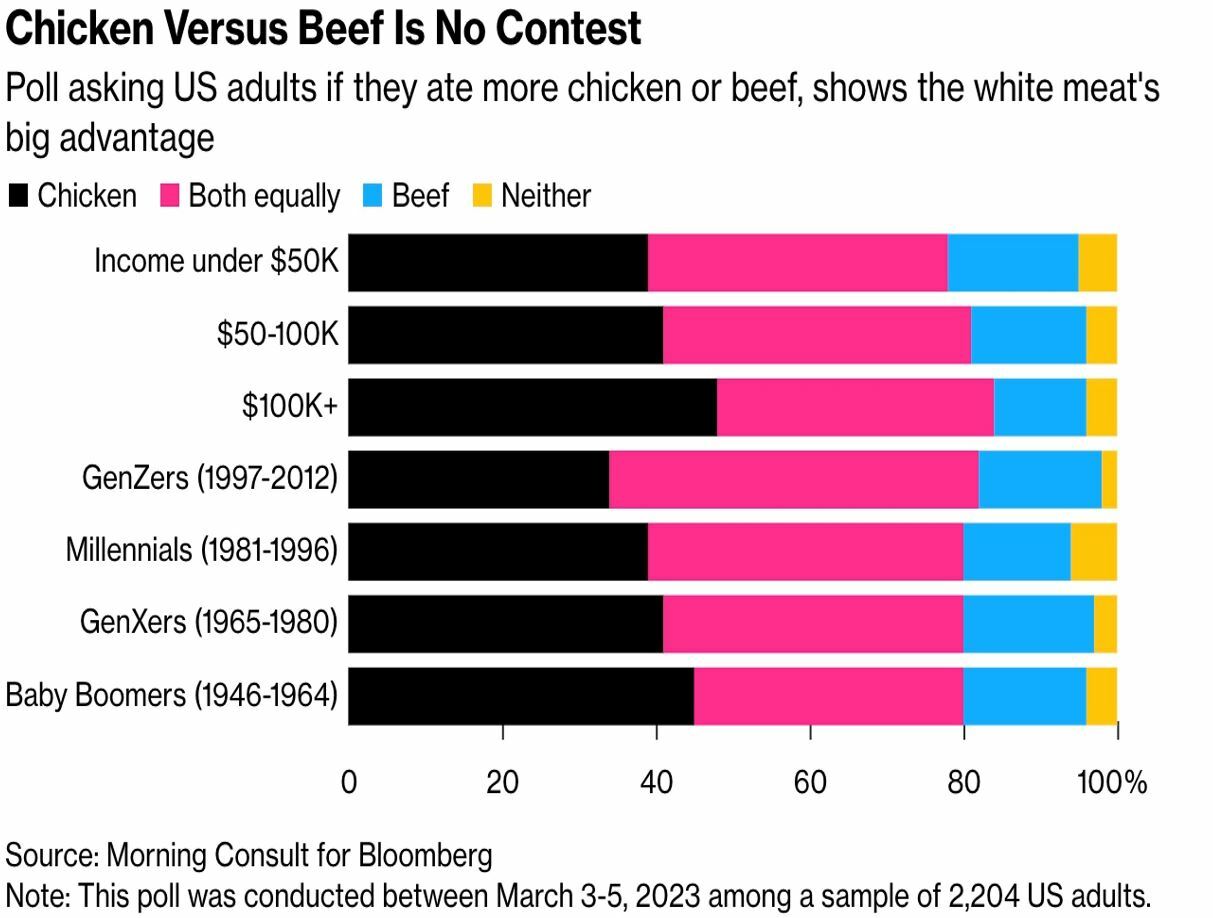

The choice for white meat is especially obvious in speedy meals and takeout, which strongly influences teenagers’ and younger adults’ consuming behavior. In 2022, white meat featured in 4 of the highest 10 pieces ordered on Grubhub, whilst pork best gave the impression in cheeseburgers.

The white meat rage is vital throughout the just about $1 trillion U.S. eating place marketplace. Chains like Chick‑fil‑A and Popeyes have thrived, even inflicting non-chicken chains to reinforce their white meat methods. In a Morning Seek the advice of ballot, 41% of U.S. adults claimed to consume extra white meat in comparison to 16% for pork, with white meat liked throughout all demographics.

Of observe: Even though white meat is fed on extra, when requested which meat they like, American citizens drew pork even with white meat. A dominant 75% cited style as their number one reason why for opting for pork, presenting a possibility for the {industry}. Then again, methods will have to be swift as other people go back to their pre-Covid routines.

Stats:

- In keeping with Technomic, Chick-fil-A places reasonable $6.8 million in annual earnings, nearly double burger-centric McDonald’s $3.6 million.

- The Pork Board spent $1.8 million final yr operating “It’s What’s for Dinner” advertisements. Mega white meat manufacturer Perdue Farms devoted nearly 20 occasions as a lot to advertising its birds.

— Grocery store pieces seeing higher costs don’t seem to be perishable items like white meat breasts or beef chops, however reasonably the ones discovered within the “middle retailer.” The time period refers to merchandise discovered in the midst of a grocery store, generally non-perishable items akin to potato chips, ketchup, crackers, cereals, cookies, paper towels, or even dish cleaning soap. Those crucial pieces that experience an extended shelf lifestyles, and don’t seem to be simply skipped by means of customers, end up to be getting costlier.

International meals costs have fallen to the bottom level in over two years

That’s in step with the U.N. Meals and Agriculture Group (FAO). The group’s Meals Value Index (FPI) recorded 122.3 issues in June 2023, appearing a lower of one.4% from Might, and a vital 23.4% drop from its file excessive in March 2022.

The fee fall has essentially been pushed by means of a decline in the price of all primary cereals and maximum vegetable oils. Primary contributing elements come with a 2.1% drop in cereal costs because of Argentine and Brazilian harvests, higher yield possibilities in positive areas of the U.S, and a three.4% decline in coarse grain costs. Wheat costs additionally lowered by means of 1.3% as a result of the graduation of harvests within the Northern Hemisphere and favorable prerequisites within the U.S., amongst different causes.

Vegetable oil costs fell by means of 2.4%, even supposing decrease palm costs have been quite offset by means of an building up in soyoil and rapeseed oil costs. In the meantime, the price of dairy and sugar went down in June, while the beef worth index remained nearly constant.

The June 2023 FPI is 3.4 issues not up to that of all the yr 2021. International meals worth inflation continues to decelerate, even supposing it stays power in some areas. However, this pattern gifts a favorable outlook, particularly for international locations that depend closely on imports to feed their populations.

In spite of long-standing traits appearing an building up in meat intake as international locations’ earning upward thrust, a shift appears to be happening. In keeping with an international agricultural outlook document, in high-income international locations like Western Europe and North The usa, in step with capita meat intake is expected to lower within the coming decade. Those international locations, constituting more or less one-sixth of the worldwide inhabitants, account for approximately one-third of the overall meat fed on international.

Extra at the document: The Group for Financial Cooperation and Building (OECD) and the U.N. Meals and Agriculture Group (FAO) point out of their Agricultural Outlook 2023-32 document that the fad of stagnation in meat intake is noticeable in maximum rich international locations. They expect poultry will delivery 41% of meat protein in 2032, essentially because of customers’ expanding sensitivity in opposition to animal welfare, environmental affects, and well being considerations during which poultry has the smallest carbon footprint.

Particularly, within the Eu Union, an ongoing shift from pork and pig meat to poultry is expected. In a similar fashion, in North The usa and Oceania — that have traditionally most well-liked pork — a vital dip in in step with capita intake is predicted.

Despite the fact that prosperous customers may eat decrease quantities of meat, international meat call for stays sturdy, in particular in lower-income international locations. The document expects a 2% in step with capita building up in international meat intake over the impending ten years, caused by emerging earning and inhabitants expansion. Meat intake, as in step with sort and tonnage, is poised to extend 15% for poultry and sheep, 11% for beef, and 10% for pork.

The analysts be expecting international meat intake will keep growing till 2075. Then again, elements like demographic traits, human well being, animal welfare, and environmental considerations may negatively affect meat intake in the longer term, with international meat call for doubtlessly beginning to fall throughout the rest of the century.

The document forecasts international agricultural and meals manufacturing to develop once a year by means of a mean of one.1% thru 2032, which is part of the expansion price seen within the decade prior to 2015. Moreover, an building up in fertilizer costs by means of 10% may lead to a 2% upward thrust in meals costs, disproportionately affecting the deficient.

Of observe: The OECD and FAO name for investments in innovation, productiveness beneficial properties, and discounts in manufacturing’s carbon depth to make sure meals safety, affordability, and sustainability long-term.

China’s sow herd contracts additional in June

China’s sow herd declined 1.68% in June in comparison with the prior month, state-backed Shanghai Securities Information reported. The tempo of the decline is larger than in prior months, suggesting that farmers are accelerating culling of sows to chop their losses.

Weekly US pork, beef export gross sales

Pork: US internet gross sales of 9,900 MT for 2023 have been down 42 p.c from the former week and 28 p.c from the prior 4-week reasonable. Will increase essentially for Japan (3,200 MT, together with decreases of 300 MT), Taiwan (1,600 MT, together with decreases of 100 MT), China (1,400 MT, together with decreases of 100 MT), South Korea (1,200 MT, together with decreases of 600 MT), and Mexico (1,100 MT, together with decreases of 100 MT), have been offset by means of discounts for the UK (100 MT). Exports of 14,000 MT have been down 21 p.c from the former week and 16 p.c from the prior 4-week reasonable. The locations have been essentially to Japan (3,800 MT), South Korea (3,300 MT), China (2,400 MT), Mexico (1,300 MT), and Canada (1,100 MT).

Beef: Internet US gross sales of 24,500 MT for 2023 have been down 6 p.c from the former week and 9 p.c from the prior 4-week reasonable. Will increase essentially for China (13,700 MT, together with decreases of 100 MT), Japan (3,800 MT, together with decreases of 200 MT), Mexico (3,600 MT, together with decreases of 100 MT), South Korea (1,300 MT, together with decreases of 600 MT), and Canada (600 MT, together with decreases of 500 MT), have been offset by means of discounts for Australia (400 MT). Exports of nineteen,300 MT have been down 46 p.c from the former week and 41 p.c from the prior 4-week reasonable. The locations have been essentially to Mexico (6,800 MT), Japan (2,600 MT), China (2,600 MT), Canada (1,600 MT), and South Korea (1,600 MT).

Weekly USDA dairy document

CME GROUP CASH MARKETS (7/7) BUTTER: Grade AA closed at $2.4800. The weekly reasonable for Grade AA is $2.4725 (+0.0565). CHEESE: Barrels closed at $1.3800 and 40# blocks at $1.3925. The weekly reasonable for barrels is $1.3506 (-0.0329) and blocks, $1.3750 (+0.0415). NONFAT DRY MILK: Grade A closed at $1.0875. The weekly reasonable for Grade A is $1.1056 (-0.0139). DRY WHEY: Additional grade dry whey closed at $0.2275. The weekly reasonable for dry whey is $0.2344 (-0.0121).

BUTTER HIGHLIGHTS: Cream is to be had right through the rustic, regardless that some contacts within the East document ice cream makers are ramping up manufacturing and are drawing on to be had provides. Contacts observe excessive temperatures within the southern portions of the Central and West areas are contributing to tighter cream availability. Butter makers within the East and West are running busy manufacturing schedules. Within the East and West, call for for butter is stable from each retail and meals carrier consumers, regardless that bulk butter call for is stable to lighter within the West. Contacts within the Central area document reasonable call for for butter, however say gross sales are assembly seasonal expectancies. Inventories of butter are to be had within the Central and West areas and are famous to be sturdy within the East. Bulk butter overages vary from 0 to ten.75 cents over marketplace price.

CHEESE HIGHLIGHTS: Milk is to be had for Elegance III manufacturing in all areas. Some cheesemakers within the Midwest document excessive temperatures, and declining milk output may motive processors within the south and southwestern states to carry milk in from different states within the coming weeks. Central area cheesemakers say manufacturing has been much less stable, because of the vacation this week, however wait for extra strong manufacturing in the course of the finish of the week into subsequent week. Northeast cheese contacts document seasonally stable manufacturing, whilst cheesemakers within the West observe sturdy to stable manufacturing. Meals carrier call for for cheese is stable within the Northeast and West areas. Retail call for is reported to be sturdy within the East, however contacts within the West say retail gross sales are stable to lighter. Western cheese exporters relay stable to lighter call for. Cheese inventories are balanced within the Midwest, and to be had to satisfy present barrel and block calls for within the West. Within the Northeast, plant managers observe sturdy cheese inventories.

FLUID MILK: Milk manufacturing and availability range right through the rustic. Contacts in some spaces experiencing upper temperatures observe a decline in output, regardless that others in some cooler portions of the rustic observe stable manufacturing. Within the Northeast, some contacts document volumes of milk are being discarded. Within the West, milk provides are to be had to satisfy production wishes, regardless that stakeholders within the Pacific Northwest and the mountain states of Idaho, Utah, and Colorado observe provides are quite heavy. Contacts within the Midwest say milk and cream volumes were abundant in contemporary weeks, however volumes are actually shifting to the southern portions of the area. Within the Pacific Northwest, call for for Elegance II milk from ice cream makers is trending upper. Within the East, contacts observe stable to sturdy Elegance II call for. Within the Midwest, Elegance III spot milk costs edged upper this week however proceed to transport at under Elegance costs. Cream multiples have been unchanged within the Midwest and West this week. Cream multiples moved upwards on the top quality for cream within the East area. Cream multiples are 1.28 – 1.38 within the East, 1.20 – 1.32 within the Midwest, and 1.05 – 1.29 within the West.

DRY PRODUCTS: Costs for low/medium warmth nonfat dry milk (NDM) moved decrease in all aspects right through the rustic. Home call for for low/medium warmth NDM is stable within the Central and West, whilst export call for is softening. In the meantime within the East, call for for low/medium warmth NDM is quiet. Prime warmth NDM costs moved decrease around the vary within the Central and East areas, and on the backside within the West. Costs for dry buttermilk held stable around the vary in all areas. Dry buttermilk call for is stable to reasonable within the West, however quiet within the East and Central areas. Costs for dry complete milk moved decrease this week. Marketplace tones stay bearish as inventories stay to be had for spot buying, and see process used to be sluggish, throughout the vacation week. Dry whey costs moved decrease on the most sensible of all regional levels, whilst the ground of each and every numerous by means of area. The whey protein listen 34% worth vary is unchanged this week. The highest of the lactose worth vary moved decrease this week, as the beginning of July signaled the shift from Q2 to Q3 lactose contracts. Acid and rennet casein markets have been quiet throughout the vacation week, and costs held stable.

INTERNATIONAL DAIRY MARKET NEWS

WESTERN EUROPE: The seasonal decline of milk output has endured throughout a lot of Europe. Quite a lot of {industry} assets recommend weekly milk collections are reducing. The decrease weekly milk volumes are stabilizing milk costs for the instant. Weekly spot milk costs have additionally stabilized or have risen in a couple of instances. Uncertainty of milk provides, for the second one part of the yr, have marketplace individuals looking to resolve marketplace course. Dairy markets, typically, are quiet as many Europeans start their summer season vacations. However there’s a bearish sentiment to markets because of the uncertainties of long run call for, financial pressures, and the continuing war in Ukraine.

EASTERN EUROPE: In Japanese Europe, there are seasonal declines in weekly milk volumes, however year-to-date milk output remains to be forward of final yr in Bulgaria, Romania, and Poland. In keeping with on-line knowledge assets, milk manufacturing in Poland has endured to develop in each and every month of 2023 when in comparison to 2022. Domestically, Poland provides Ukraine with 69 p.c in their contemporary dairy imports. Because the 2023/24 grain export season starts, industry officers observe decrease volumes of grain getting exported from Ukraine. Whilst the season is best within the first few days of the brand new season, officers say grain shipments are about part of what used to be exported final yr throughout the similar length.

OCEANIA: NEW ZEALAND: Following the hot approval from the Eu Council, the loose industry settlement between New Zealand and the Eu Union has moved nearer to finishing the contract as early as subsequent month. There’s competition from some Eu farmers who say the deal may motive a flood of New Zealand dairy merchandise into Eu dairy markets. In the meantime, New Zealand dairy export volumes and values for Might 2023 display an building up for all primary dairy commodities.

AUSTRALIA: Welcome information for the Australian dairy {industry} used to be the Might milk manufacturing document, which underlined a 1.6 p.c, year-over-year, building up in output. The rise used to be the primary per 30 days expansion seen this quick season, as harsh climate and dairy {industry} constraints restricted milk manufacturing output. In the meantime, Australian April dairy exports posted some no longer so welcome figures, as general dairy export volumes declined 25 p.c, in comparison to a yr in the past.

SOUTH AMERICA: Reviews display blended milk output in Brazil throughout the primary quarter of the yr, however Argentine and Uruguayan experiences are a bit extra stable month to month. Obviously, the lengthy and protracted drought, which has eased regardless of contacts proceeding to document some relative contemporary dryness, has performed an element in holding milk output in take a look at. That mentioned, near- and mid-term expectancies are starkly other from the ones of earlier years from regional contacts in regard to later iciness/early spring milk output. Farmgate milk costs have higher because of the volatility/limits of milk manufacturing. Feed costs are nonetheless particularly upper, in comparison to pre-drought years, because of crop obstacles caused by drought prerequisites till the previous few months. Brazil remains to be a primary vacation spot for dairy commodity exporters in Argentina, Uruguay and Chile. That mentioned, as Brazil’s milk manufacturing expectancies have garnered power, there are tell-tale indicators that their iciness/spring buying will ebb. Costs of dairy powders are starting to fall in keeping with globally bearish values.

NATIONAL RETAIL REPORT: Overall typical advertisements declined by means of 12 p.c on this week’s survey, and general natural advertisements declined by means of 41 p.c. In spite of showing in 19 p.c fewer advertisements than final week, ice cream in 48-64-ounce boxes remained probably the most marketed typical dairy product for week 27. The weighted reasonable marketed worth for this merchandise declined by means of 29 cents to $3.59. Natural ice cream in 48-64-ounce boxes gave the impression in 172 p.c extra advertisements on this week’s survey and had a weighted reasonable marketed worth of $7.99. The natural top rate for ice cream in 48-64-ounce boxes is $4.40.